Greetings! I trust the new year is treating you well. As we embark on the journey through 2024, it's essential to keep a close eye on prevailing trends and market conditions that shape our economic landscape. Let's delve into some key considerations and strategic insights for the early months of this year.

Key Trends to Watch in Early 2024

1. Interest Rates and Employment:

The market's anticipation of interest rate cuts puts a spotlight on jobs data. Strong employment numbers are generally positive for the economy, but in the context of expected rate cuts, we would like to see some softening here. It will not be a popular talking point for politicians – they’ll focus on either ‘creating jobs’ or ‘fighting inflation’. The reality is that fighting inflation means you are also seeking to slowdown the job market.

2. Consumer Price Index (CPI) Readings:

The gradual cooling of CPI readings is encouraging. The lagged impact of the Fed’s interest rate hikes seems to be providing a potential reprieve from inflationary pressures. The chart below displays an inflation heatmap where dark red indicates strong inflationary pressure while blue indicates slowing/cooling inflationary pressure2. Each 'block' indicates one quarter of data plus we have the monthly data in the two columns on the far right.

3. Housing Trends:

Residential real estate, a significant component of our standard of living, is near all-time highs. While the recent increase in mortgage rates has led to decreased demand, finding a delicate balance is essential. Too much of a slowdown in real estate could push the economy into a recession. We'll be watching the monthly data closely.

Positioning the Portfolio to be Nimble

In navigating these trends, our approach is centered on adaptability. The Federal Reserve aims to see a moderate slowdown without veering into recession territory; however, the Fed does not have a solid track record of engineering a so-called soft landing. Nonetheless, the market is expecting exactly that scenario.

Our portfolio remains balanced. Over the last several weeks, we have increased our allocations towards hedged equity and stable value. These slices provide us with flexibility in a down market, while also giving us some yield and upside potential in flat-to-rising environments.

Update on Recent Tactical Adjustments

The slices above were funded from sales of several tech positions in the portfolio. In December 2023, we trimmed positions in cutting-edge technology. Collectively, these positions saw large price increases in 2023 on the back of AI-driven excitement. Our exit, guided by daily monitoring using the Relative Strength Index (RSI)3, was prompted by overbought sentiment and changing interest rate expectations.

The tech positions we sold have declined over 10% in the handful of weeks since our exit. If the weakness continues, we remain vigilant for an opportunity to reverse back into these positions – of course, this would be at lower levels than our recent exit prices.

Geopolitical Events: A Critical Lens

Heightened tensions in key geopolitical regions demand our attention. Two areas of focus include:

1. Russia/Ukraine:

As major exporters of grain, these countries play a crucial role in global food supply. Grain is used in many different foods around the world plus it’s a primary feed for various livestock. Escalating tensions could lead to ripple effects that increase food prices globally.

2. Israel/Gaza + the Broader Region:

The potential for expansion into broader regional conflict has serious implications, especially for the energy markets. Recent actions by Iranian proxies, such as the rebel group Houthis, in the Middle East add complexity to an already delicate situation. There attacks on the Red Sea are causing merchant vessels to reassess their shipping lanes. A longer route around Africa will increase shipping costs for a significant percentage of global trade. See the map below as to why the new shipping route contributes to increased shipping costs. Vessels would have to sail around the southern tip of Africa rather than through the Bab al-Mandab Strait:

What’s the bottom line?

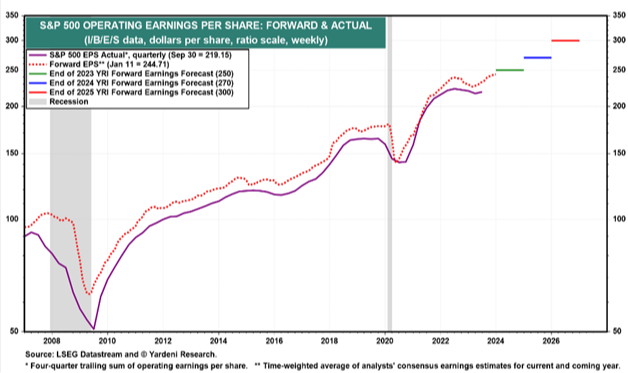

It’s likely you are picking up on a cautious tone as you read this article. With this said, we are NOT particularly bearish in 2024. If the economy can avoid recession, then we should see continued earnings growth. The chart below, sourced from Yardeni Research4 —a reputable provider of economic data and forecasts—displays S&P 500 earnings estimates.

Here are the earnings estimates for each calendar year:

2023 – 250 points

2024 – 270 points

2025 – 300 points

If these estimates are met, then 2024 represents 8% earnings growth over 2023. 2025 would be a 20% increase from 2023. The intermediate term trend and long-term thesis for the stock market remains strong – earnings growth is a key driver of stock market performance. Our concerns are largely near-term, which is why our mantra for 2024 is “staying balanced”. If the herd runs too far in one direction or the other, then we often find ourselves making attractive tactical adjustments – all while staying balanced.

Disclosures:

1. Investment Advisory Services offered through Cobblestone Asset Management, a Registered Investment Advisor. Securities offered through Independent Financial Group, member FINRA/SIPC. Cobblestone Asset Management and Independent Financial Group are separate and unaffiliated entities.

2. Source: Bank of Mexico, Central Bank of Brazil, DGBAS, Eurostat, FactSet, Federal Reserve, IBGE, India Ministry of Statistics & Programme Implementation, Japan Ministry of Internal Affairs & Communications, J.P. Morgan Economic Research, Korean National Statistical Office, National Bureau of Statistics China, Statistics Canada, Statistics Indonesia, UK Office for National Statistics (ONS), J.P. Morgan Asset Management. Heatmap is based on quarterly averages, with the exception of the two most recent figures, which are single month readings. Colors determined by percentiles of inflation values over the time period shown. Deep blue = lowest value, light blue = median, deep red = highest value. DM and EM represent developed markets and emerging markets, respectively.

Guide to the Markets – U.S. Data are as of January 12, 2024.

3. The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is used to identify overbought or oversold conditions in a financial market, helping traders assess potential reversal points.

4. https://yardeni.com/charts/sp-500-yri-forecasts/ -- figure 4